Go back to

Part 0.

Introduction to Property Market Analysis - Demography

Sarawak and Sabah are two state of Malaysia where land is in abundance. People in these two states are opening up to new technologies (broadband is reaching 3G to most of the townships). Furthermore, urbanization is slowly and surely taking over the capital cities and key townships. The young generation (GEN Y) are now maturing into work force, either seeking employment in the cities (KL, Singapore, HongKong etc) or remain in the State but moving to Kuching and Kota Kinabalu instead of staying back in small towns. They will return to their home towns and influence their elders with regards to the perception of the property market, be it investment or own use.

In short, demographic changes is rapidly underway, and urbanization will influence the cities and the suburbs towards the perception of property investment. On one part, the demand for own use, and on the other part (which is more premium) the demand for investing into properties.

The GEN Y provides the never ever ending demand for properties. Take for example, based on the number of SPM candidates - 2014 the figure is at 455,839 (whole Msia) and 37,488 (Swk) and 32,197 (Sbh).

A conservative estimate of 10% of the market would be 3,500 houses per year if only 10% of them are getting married and starting their family. This has not include the population one year before or after which are likely to be married too! A very conservative guesstimate would be 3,500 x 3 = 10,500 houses in demand at any one time! An average of 4 years' data is analyzed below in Figure 1.

Figure 1

Similarly, UPSR candidate numbers are not far from this, Figure 2 below shows the number of candidates who sat for UPSR over a 4 year period from 2008 - 2011.

Figure 2

Therefore, from the analysis of UPSR and SPM candidate numbers, we know that about half a million of students will leave the schools to seek for work every year. They will be in preparation to own a property in the near future - 3-5 years (an assumption to be studied). This means that an estimated new household of 250,000 a year. Even taking a mere 10% of this figure, the demand for housing in Malaysia is around 25,000 a year!

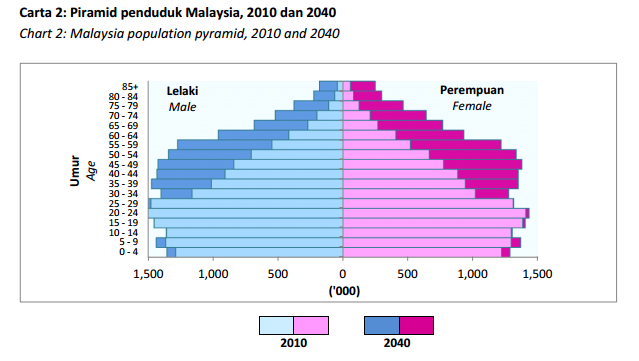

Cross checking with the data from the 2010 Population Census, see Figure 3,

Figure 3

the age group 15-19 years old from the 2010 population census was 1.4 mio male and 1.3 mio female. This is a combined 2.7mio over 5 years. Hence, the average population is around 540,000 per age group.

This figure is near to the yearly total student population sitting for UPSR or SPM. Thus, the figure is accurate for our consideration.

Future age distribution is been projected as below.

The discussion on the age distribution pattern will be done in

Part 3 - Demand here.

Supply and demand analysis is commonly carried out by developer and investor to guide them on their portfolios.

Demographic analysis on numbers of SPM students may be indicative of the demand pressure. However, other factors like locality and socioeconomic status or purchasing power of the population are as important if not more so. Imagine a huge poor population like in Africa or India during the early years, they could not afford food, what more talk about housing. They had to stay in slumps. In the countryside, they built their own huts, and demand for constructed housing was either too few, or unimaginable. It was of course never any thoughts of high rise apartments or condominiums.

On one side it is easier to estimate supply because it is tangible (Hamid, 2007). That means developers can come out with plans and maps of development projects, whereas demand is difficult to estimate because there are too many assumptions. From the supply side, there are three (3) main types of property supply (Hamid, 2007), namely planned supply, incoming supply and existing inventory.

On the other side of demand, it is harder to estimate (Hamid, 2007). Firstly, one never know with certainty how buyers would respond to a new development. Nobody really knows what exactly the buyers consider in making decisions pertaining to buying, renting or patronizing a newly proposed property project. No one knows the competition would be like against a new project in the future. In other words, there is a lot of uncertainty and unknown demand outcomes to the developer or investor.

Thus, most property demand is based on bird's eye estimates. From analysis of past trends, certain secondary data can probably indicate increasing demand in certain property type. However, whatever accurate it may be, it is still an estimate as conditions may have altered as time passes by. A trend of property with large door and windows might be outdated now, as well as a locality previously command a premium might now be deserted due to reasons like congestion or rampant theft problem.

Owing to this assumptions, it is very much limited to general trend as if the market is moving upwards for apartments because of affordability, and bungalows and luxury land is moving downwards due to economic slowdown. Inflation and loan availability are also factors which can affect property demand.

Due to assumptions above, the analysis would base on current available properties, potential new developments published by National Property Information Center (NAPIC) under the JPPH.

Analysis of Property Market

This section is about different aspects of property market. Analysis covers:

Part 2 Supply

Part 3 Demand

Part 4 Historical analysis*

Part 5 competitive analysis

These various analyses are posted on later parts.

*value transacted and frequency of transactions.

Continue to Part 2 here.

Ref:

Abdul Hamid Mar Iman. 2007. Property Supply and Demand. Penerbit UTM. Page 25-41.

The Sun Daily. 03.11.2014. 455,839 candidates sit for SPM today. Available at,

http://www.thesundaily.my/news/1216096

Borneo Post. Antonia Chiam. 04.03.2015. 15 in Sarawak score straight A+ in 2014 SPM examination. Available at,

http://www.theborneopost.com/2015/03/04/15-in-sarawak-score-straight-a-in-2014-spm-examination/

Daily Express.04.03.2015. SPM: Fewer students scoring all As. Available at,

http://www.dailyexpress.com.my/news.cfm?NewsID=97561

Population Census 2010 , available at

http://www.statistics.gov.my/portal/index.php?option=com_content&id=1215

Population Projection Malaysia, 2010-2040. Chart 2; page 3. Available at,

http://www.statistics.gov.my/portal/download_Population/files/population_projections/Population_Projection_2010-2040.pdf